Ultimate Guide For Final Expense Life Insurance

Although it is never too early to begin making plans for the future, it can be challenging to know where to begin. We are prepared to assist.

Everything you need to know about last expense life insurance, including how much coverage to acquire, who should buy it, and what inquiries you should have before buying, will be covered in this book.

Get the information now so your family won’t look back and regret it later.

What is a Final Expense Insurance Policy

Seniors favor final expense insurance because it is a sort of simplified whole-life policy that pays for funeral and medical costs when the insured goes away.

Because the majority of plans include these components, it is often known as burial or funeral insurance.

As long as the insured person makes the necessary monthly payments, whole life insurance offers protection for the duration of the insured’s life. A policy’s cash value can build up if premiums are paid.

Until these policies are payable-in-full (PIF) or insureds can withdraw money utilizing a policy loan, fixed premiums are charged.

Simpler issues only ask applicants to respond to health-related inquiries during the application process; no medical examination is necessary.

Whole life insurance makes sense for those who require financial aid later in life and cannot wait months to receive significant sums of money from conventional sources like bank loans or credit cards because it has quick approvals and inexpensive rates.

Final Expense Life Insurance For Seniors

Seniors frequently choose last expense life insurance due to its low cost and lower payout amounts.

The policies concentrate solely on this element rather than attempting to make up for any lost income due to a person’s death because they are generally used to pay for funeral expenditures.

Since they have already paid off their mortgages and have no dependent children, retirees do not require life insurance.

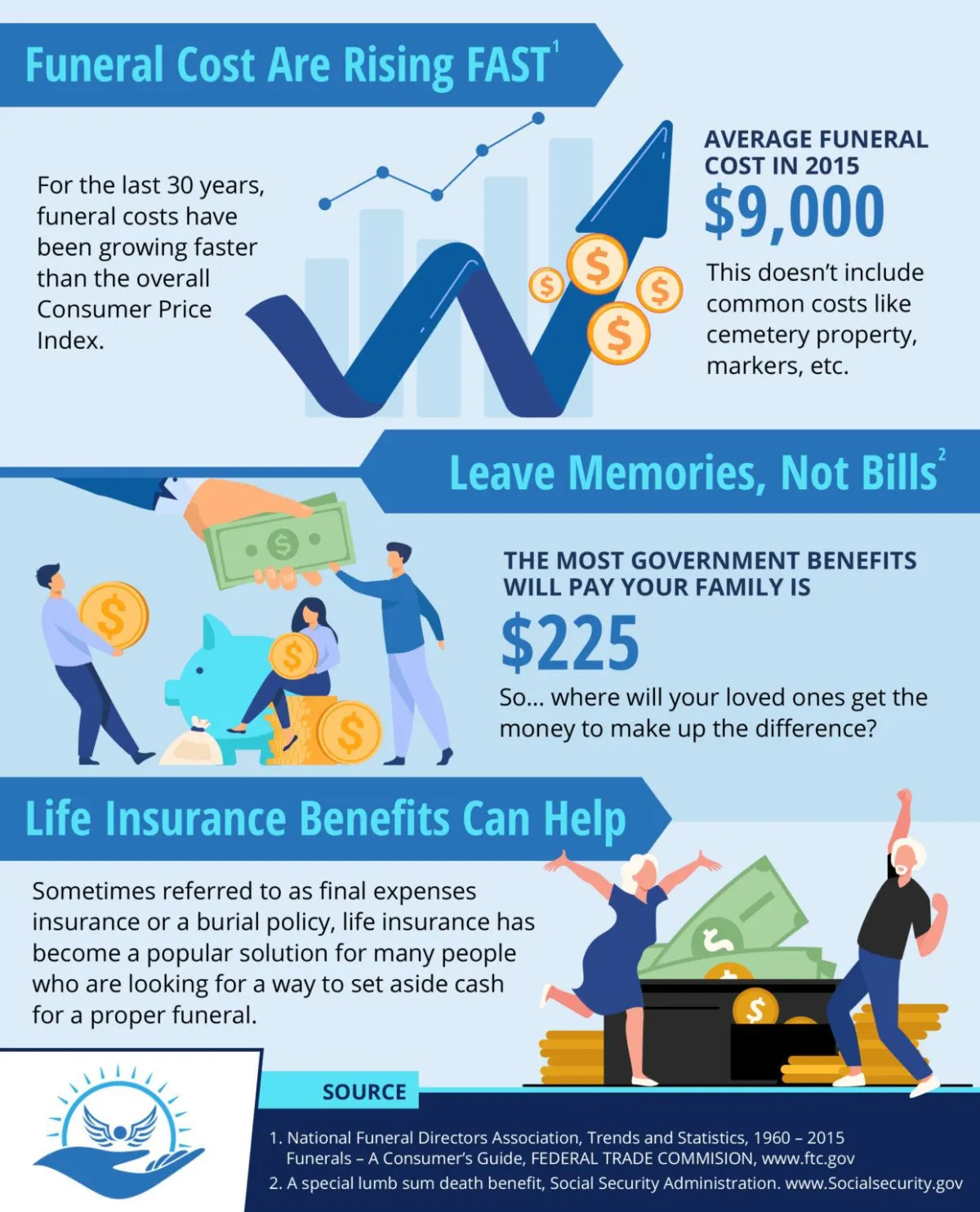

However, when someone passes away, they may leave behind hefty debts; the National Funeral Directors Association estimates that only the cost of the funeral may exceed $9,000. (NFCDA). For this reason, it’s crucial for retirees to make investments that will pay for these final expenses after death.

If you’ve ever dealt with a loved one’s death, you are aware of how difficult it can be. Planning a funeral and dealing with your grief may consume all of your time, in addition to any financial commitments that need to be fulfilled.

The prospect of our partners or kids going through the same thing after we pass away is terrible. So what does this have to do with last expenditure life insurance? When we don’t return from heaven, this sort of protection will make sure they aren’t left with mountains of debt.

Seniors who want to shield their loved ones from the escalating funeral costs may consider purchasing burial insurance. Because they’re based on health-related questions, they’re typically fairly simple to get—in many circumstances, you don’t even need a medical checkup!

How Much Does Final Expense Insurance Cost (Sample Rates)

The table below demonstrates that rates are lower when a person is younger. As a result, many seniors enroll in insurance as soon as possible to lock in inexpensive rates before they significantly increase with age or a medical condition.

Common Questions You May Have About Final Expense Life Insurance

Even though it is frequently simpler to qualify for a final expense coverage than for other sorts of life insurance, there are still crucial inquiries to make, such as:

How do I know when my final expense insurance expires?

Term and whole life insurance are the two categories into which they fall. Because final expense policies are a subset of whole life insurance, as long as you keep making on-time premium payments, your coverage will never lapse!

Can I get life insurance without a medical exam?

It’s possible that you won’t need to take an exam if you only need a little quantity of coverage, such less than $50,000. Smaller amounts of insurance typically rely on applicants’ responses to questions or interviews rather than actual medical examinations.

What features are included in a final expense policy?

The life insurance provider will determine the final expense policy you select. Some businesses also provide coverage for minor riders, accidental death, and dismemberment.

Review each benefit carefully before selecting one if your goal is to design a policy with additional protection against all hazards that might develop after your passing because they are not always included in every single plan offered by various insurance providers.

What can the death benefit from a final expense insurance policy be used for?

Even though final expense insurance is designed to pay for funeral expenses, the death benefit can be used for any purpose, including paying off debt from credit cards, mortgages, or medical expenses.

Your recipient finally decides how to use the death benefit, so they can be sure it won’t be wasted.

What is The Average Cost of Final Expense Insurance

Prices for ultimate expense policies come in a wide range. The average cost ranges from $30 to $70 each month, although it varies depending on your age and any underlying health issues, including diabetes.

Expect to spend between $70-$120 a month if you are over 70 or have serious health issues, though rates within or outside of these ranges may be offered.

Younger candidates who do not have any significant medical conditions may be eligible for premiums at the low end of this range, which range from $20 to $50 per month. However, keep in mind that a lower price typically translates into fewer features and advantages for survivors.

Gaining a few extra bucks here could have a significant impact on the level of support your family will get following your passing.

It’s crucial to consider what else you’ll be accountable for in addition to how much the insurance will cost. After a loved one passes away, there may still be debt from credit cards and hospital costs that must be paid by the family.

Below, we’ll go over each of these expenses:

Cost of Medical Bills

Eighty percent of the 2.6 million Americans who passed away in 2014 were beneficiaries of Medicare.

The cost of healthcare was more than anticipated because chronic illnesses necessitate costly medical treatments and because health insurance frequently does not cover a person’s needs in the final year of life, when hospitalizations and hospice care incur large costs.

Only two-thirds of the costs for older patients’ healthcare are covered by Medicare and Medicaid. Each person spends $18,424 on healthcare annually.

For hospice care in 2016, Medicare spent an average of $153 per day. This comprised:

Routine home care costs $193.

$41 for ongoing home health care

$173 for short-term care

standard hospital services costing $744

Final Charge Families can safeguard themselves against any unforeseen medical expenditures incurred by their loved ones, who might not be able to afford the price of end-of-life care, by purchasing life insurance.

Final Expense Insurance Can Take Care Of The Debt Left Behind

An average American dies with debts of approximately $61,554. Before transferring any assets to surviving family members, the estate pays off as many obligations as it can. It is the cause of death for 73% of Americans.

These may consist of:

25,391 of the average person’s debts are student loans. This indicates that a lot of students are taking on a lot of debt to cover their educational expenses. However, because student loan installments can be fairly high and college is highly pricey, they might not have enough money left over once everything has been paid for.

Debt incurred for 17,111 dollars is made up of auto loans.

14,793 are personal loans, and $4,531 are credit card obligations.

Even while funeral costs and other expenses may cause family members to need additional money after a loved one passes away, the majority of people owe over $100,000, so it seems like there isn’t much left over when all these transactions are removed from someone’s bank statement.

Term life insurance is the most popular kind and its face value can reach millions. A final expense insurance, on the other hand, is often around $20k and simply covers the cost of making funeral arrangements.

Families are unaware that the average expense of a funeral is $9,000 or more. By providing an exact sum rather than speculating on how much money a loved one would require for all expenses, final expense insurance can help lessen the emotional cost of overpaying on a relative.

It Does Cover Funeral Costs (Funeral Cost Breakdown)

In 2017, the average price for an adult funeral including viewing and burial was $8,755.

Depending on the casket’s material or the cost of opening and closing the grave, funeral expenditures might run into the thousands.

Because of this, insurance firms provide final expense plans—often referred to as “funeral” or “burial” insurance policies—to pay for these expenses.

Over the years, there has been ample documentation of the escalating cost of funerals. The cost of a funeral without a vault had increased from $700 on average in 1960 to at least $7,640 in 2019, with grave markers costing an average of $200 to $400 per and additional costs for obituaries or memorial services pushing the total closer to $10,000.

Shopping For A Final Expense Insurance Quote Online

The price of last expense insurance depends on a variety of elements. The most economical coverage with one provider may not be the greatest choice for you when compared to another policy because every company calculates rates differently.

Speak with an agent who, because they are familiar with all of these firms, can give you free quotations depending on your needs and requirements to help you decide which is best for you.

A final expenditure plan should be chosen after answering a number of key questions.

How is the provider going to safeguard your family? What is the typical time it takes to pay claims? Do they plan to pay for your funeral or will they leave it up to you and your loved ones?

One can only choose the business that gives them peace of mind during this trying period after taking these considerations into account.

Hassan Sanders, the founder of DiabeticInsuranceSolutions.com, has been specializing in final expense life insurance since 2008. He is renowned for his company’s quick application process, which only needs applicants to answer a few health-related questions on a one-page form; there is no need for a medical exam.

But what really distinguishes us from other service providers is the support we offer in the event that the policyholder passes away. Since there is less stress during such a sensitive moment as losing a loved one, we assist in easing the process when it comes to making burial arrangements.

What are the Pros & Cons of Final Expense Life Insurance

With a final expense coverage, you can spare your loved ones the stress of paying for your exorbitant afterlife needs. It is hardly surprising that funeral expenses generally run far over $10,000 as casket expenditures alone can range from $1,000 to $10,000 depending on style and material.

Getting a more affordable final expense plan will protect those closest to you from such an unfortunate event occurring in their lives as well. Families frequently experience financial burdens as they prepare for funerals if left unpaid or unplanned for by life insurance policies, which is why getting one will protect you.

A sort of permanent insurance policy is whole life insurance. The death benefit and premium for the majority of conventional whole life insurance policies stay the same for as long as you keep the policy; some build up cash value.

Because whole life insurance lasts until your death rather than having an expiration date like term or temporary insurances do, it is frequently referred to as “permanent” insurance.

Funerals often cost between $10,000 and $20,000 on average. Because it doesn’t need to cover the same range of expenses as regular life insurances do and only covers lesser sums for funerals, a final expense policy is less expensive than other insurance policies.

Most importantly, last expense insurance have lower coverage levels, making it simpler to qualify for them. They can be granted based on answers to health-related application questions without the need for a medical test.

The biggest disadvantage of a final expenditure policy is that it has a significantly lower face amount than other types of life insurance, like term.

But bear in mind that beneficiaries can use it for anything, so you could even purchase a policy to aid with funeral expenses and then later receive reimbursement from them!

Why Do You Need Final Expense Insurance

For people over 40 who need money to pay for their final expenses and funeral fees, final expense life insurance may be a good option.

Since the benefits are often lesser than those of other types of coverage, this sort of policy typically has lower premiums than regular plans and a death benefit between $5,000 and $20,000 (and more as you age).

If premiums are paid on a monthly basis, a permanent life insurance policy that does not expire builds up cash value over time.

The benefits of this sort of insurance won’t have an expiration date and can mount until they outweigh its costs, which are often quite long term from the perspective of policyholders, making it an appealing alternative for seniors wanting to cover their final bills.

Anyone over 50 who wishes to safeguard their loved ones in the event of their death can purchase an affordable life insurance policy. Life insurance is not just for the old.

Children may also purchase a life insurance policy on their parents or grandparents. Obtaining many quotations, including one that covers funeral expenses, will help you decide which kind of coverage best meets your needs.

This might not apply if you have a sizable sum of money set aside to pay for funeral expenditures out of pocket or if you’re receiving hospice care and are therefore ineligible for last expense insurance.

If not, nothing would prevent the government from rejecting your claim.

Who Is Final Expense Insurance Best For

There is no better choice for senior citizens when it comes time to buy life insurance than last expense coverage. This kind of insurance focuses on paying for funeral fees and other last expenses that may be difficult for surviving loved ones to afford following the death of a family member or acquaintance.

The focus on funeral arrangements makes these products identical to burial insurance, which you may have seen marketed.

Final expenses are also reasonably priced (often don’t require a medical exam), which makes it simpler for senior consumers to make selections about new financial products since they don’t always think about their money.

How Do You Apply For Final Expense Life Insurance

A brief application is needed for each life insurance coverage. It may be between one and two pages long and ask you questions about your height, weight, family history of illnesses, or regular activities.

Other businesses have longer applications with numerous health-related inquiries that call for diagnostic procedures like blood and urine tests.

The applicant does not need to undergo any tests in order to be accepted by the company’s requirements because DiabeticInsuranceSolutions.com just asks the basic health-related questions, unlike other businesses.

Depending on the type of insurance, the application procedure can vary, but you will typically need to complete a form online or over the phone.

Your insurer will provide you a free estimate, and it ought to include all applicable savings. In certain circumstances, policies can be sold over the phone without further interaction being necessary;

Face-to-face discussions are still advised in these situations before acquiring any policies because it’s possible that more questions will be resolved then.

What Are the Pre-Qualifying Questions

The majority of final expenditure applications ask about the timeline, above all. In actuality, most final expense providers simply consider the prior two years. Here are a few of the most often asked queries about pre-existing conditions.

Have you ever had one of the following diagnoses:

HIV/AIDS, bedridden, in a care facility, hospitalized, or getting hospice care?

Do you suffer from a heart condition like congestive heart failure or a stroke?

have abused alcohol within the last two years.

Has it been more than two years since you received a cancer diagnosis?

Alzheimer’s illness

You may have an answer to one or more of the following queries.

Even if your health has deteriorated, do you want coverage?

Do any members of your family rely on your income to make ends meet?

Is last expense life insurance a reasonable way to pay for funeral costs and other death-related obligations, such as unpaid medical bills or debts left by surviving family members?

Do you suffer from conditions that preclude coverage, such as type 2 diabetes? Most people can obtain coverage with last expense life insurance even if they’ve had health issues in the past.

What Are The Coverage Levels For Final Expense Insurance

The typical policy is closer to $10–20k, although the majority are under $50,000. If you qualify for an adjusted plan, the cost may be lower than a typical final expense policy depending on your health and the types of coverage you select.

A modified plan with an extended waiting period is given to the applicant. If the insured survives, they will receive a full refund of their premium payments plus a little loyalty incentive.

To accommodate the requirements and financial constraints of the deceased, the final expense sector provides a variety of plans. Some businesses allow applicants to pay their policy in full within ten years by offering 10- or 20-year payment plans.

These will have greater premiums than other plans, but they are less expensive because they include charges for burial expenses like casket and vault fees.

Insurance Tips For End Of Life Preparation

When the time comes, coverage denial due to lying about your health or medical history.

It is best to provide complete and honest answers when applying for end-of-life insurance. Since businesses will probably study the records after a person passes away to determine any differences between what is written down and what occurs in person, being honest is essential!

It’s crucial to prepare in advance and be aware of local funeral expenses. Any local funeral home should be able to provide you with a general cost list, which will give you an idea of how much final arrangements may end up costing your loved ones.

It’s also useful if the person handling your affairs has copies of all pertinent paperwork. Share your preferences for flowers or music during the funeral as well, for convenience’s sake, so loved ones won’t have to guess your final desires at the last minute.

It’s crucial to regularly examine your insurance so you have adequate cash to provide for surviving family members.

Funeral expenses are always rising, and life insurance is not an investment that can be made once.

Your health could unexpectedly change as you age! When it comes to safeguarding those who depend on us the most for existence, it pays off in spades.

What Types Of Beneficiaries Are There

When you pass, who gets to receive your life insurance benefits?

There are three main types of beneficiaries:

Primary (the first person the insured names as a beneficiary),

Contingent (if something happens to the first two within 30 days after death), and

Tertiary

They will call in Tertiary Beneficiaries when it’s time for someone else to be informed about getting money from an account besides these individuals or groups who depend on one another for survival.

You can divide your death benefit in a number of ways, but it’s crucial that you define the proportions that each beneficiary should get.

So that there is no misunderstanding when the time comes, let these people know in advance what percentage they will receive!

It is crucial to name your adult children as primary beneficiaries on your life insurance plans as this will make the death benefit distribution simpler.

Make sure you include pertinent details about them (their address, phone number, and birthdate) so that an insurance company representative can quickly confirm their identification in the event that a claim needs to be filed.

It’s crucial to carry life insurance, but it’s even more critical to keep your beneficiaries informed. Additionally, you must constantly let them know if your phone number or address changes so they can update their information.

Are Pre-Paid or Pre-Need a Good Option

Check to see how the funds will be stored and what services they can cover before prepaying for your funeral. Keep thorough records because if you order the service in advance, you might be able to lock in a particular price.

Pre-paying for a funeral isn’t always a wise decision, and you need to understand how it works in detail.

Because the prepaid plan can only be used to cover funeral expenses and not other desired wishes, it typically offers less flexibility than last expense insurance (ex: cremation).

When employing this payment method, for instance, a person will forfeit all of the money paid if they move or change their goals (for instance, they decide they wish to be buried).

Conclusion

Despite the fact that we’ve provided a thorough overview, if you know someone who might require last expense life insurance and would like more information on their best possibilities, we can help. Call us at (855) 468-8900 right away, or fill out the form on the right, and we’ll contact you with a free quotation right away.

Remember that last expense life insurance policy coverage varies from company to business, so it’s always a good idea to check pricing before making any decisions if you’re reading this page in search of general information. People can learn how crucial planning ahead can be by using the power of hindsight, especially when it comes to financial matters.